The Department of Finance, vide its Gazette dated 18th January 2022, has made effective the Income-tax (2nd Amendment) Rules, 2022, introduced therein, adding rule 8AD, enumerating computation of capital gains for sub-section (1B) of section 45, which has been made effective from A.Y. 2021-22.

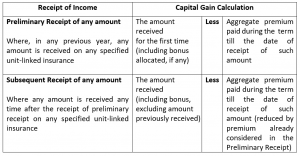

Section 45 (1B) has introduced taxability as a capital gain for any amount received under a unit-linked insurance policy, which is not exempt under section 10 (10D), including the bonus received. Rule 8AD provides for computation methodology for capital gains on a specified unit-linked insurance policy on initial receipt and subsequent receipt of any amount under such policy.

As per the Gazette, these capital gains from receipts under specified unit-linked insurance policies shall be deemed to be capital gains from the transfer of a unit of an equity-oriented fund set up under a scheme of an insurance company comprising unit-linked insurance policies.

#finance #insurance #tax #capitalgainstax #globalconsulting #financemarket #financeleadership #financeandaccounting #industryinsights #industryexperts #insuranceindustry #policy